Managed TMS Services vs Software Procurement: The European Cost-Benefit Framework That Prevents €500K+ Implementation Disasters

European procurement teams evaluating transport technology face a dangerous blind spot. While you debate features and integration timelines, 75% of European TMS implementations are failing their budgets, with software license typically only 20-25% of total cost of ownership. The hidden reality? Budget overruns hit 75% of European TMS implementations, and 66% of technology projects end in partial or total failure.

Your traditional procurement framework comparing vendors by subscription costs misses the point entirely. A German automotive parts manufacturer discovered their €800,000 TMS implementation mistake the hard way. Six months into deployment, they found their European carriers couldn't integrate without costly custom development work - transforming their calculated software purchase into a complete platform re-implementation.

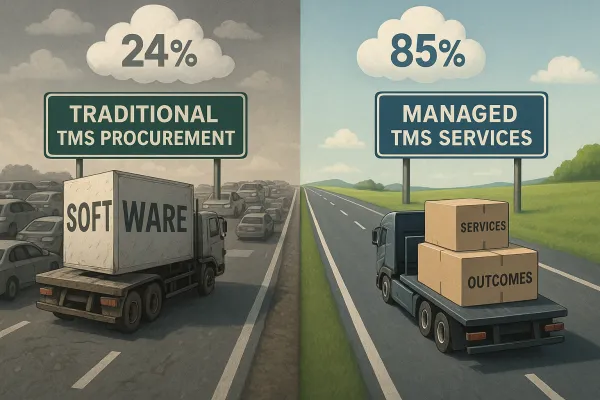

Meanwhile, a quiet revolution is reshaping European transport procurement. The services segment is projected to expand at a fastest CAGR of 11.4% from 2026 to 2034 owing to the increasing complexity of TMS deployments, the need for continuous system customization, and the rising demand for managed services. The mathematics are compelling: when hidden costs (invoice leakage, spot overpayment, coordinator time) are included, managed transportation is typically less expensive at $3M+ freight spend.

Why European Shippers Are Abandoning Traditional TMS Procurement

Europe's ICT professional deficit exceeding one million workers is forcing a fundamental rethink of transport technology strategies. European manufacturers are discovering that a basic domestic shipper requires 10-15 integrations minimum, potentially totaling 1,000-1,500 hours of labor. For shippers with freight spend exceeding $250M annually, implementation can cost 2-3 times the subscription fee.

The numbers reveal the crisis clearly. Industry analysts estimate total cost of ownership for a mid-market TMS at 2-3x the quoted software price over a 3-year period. When you factor in mandatory European regulatory compliance - basic API integrations cost €5,000-€15,000, while complex ERP connections exceed €50,000 - traditional software procurement becomes a financial gamble most procurement teams cannot win.

Consider the regulatory timeline pressure. From July 1, 2026, vans weighing 2.5-3.5 tons performing international transport of goods will be subject to the obligation to use second-generation smart tachographs (G2V2). Simultaneously, as of 1 January 2026, the transitional phase of the Carbon Border Adjustment Mechanism (CBAM) has ended, with importers now subject to full financial obligations under the scheme and €100 per excess tonne penalty for non-compliance.

The Managed TMS Services Value Equation

The break-even analysis reveals why procurement teams are pivoting. The break-even is approximately $5M freight spend: Below $5M, self-managed freight with 1 coordinator is often cheaper in hard dollars; above $5M, the hidden cost gap typically closes the advantage. Managed transportation typically delivers better total cost outcomes at $3M-$5M+ freight spend.

Timeline advantages compound the financial benefits. A managed transportation transition takes 60-90 days. A TMS implementation typically takes 6-18 months. In an environment where as of 9 July 2027, the eFTI Regulation will apply in full, speed becomes a competitive requirement, not a preference.

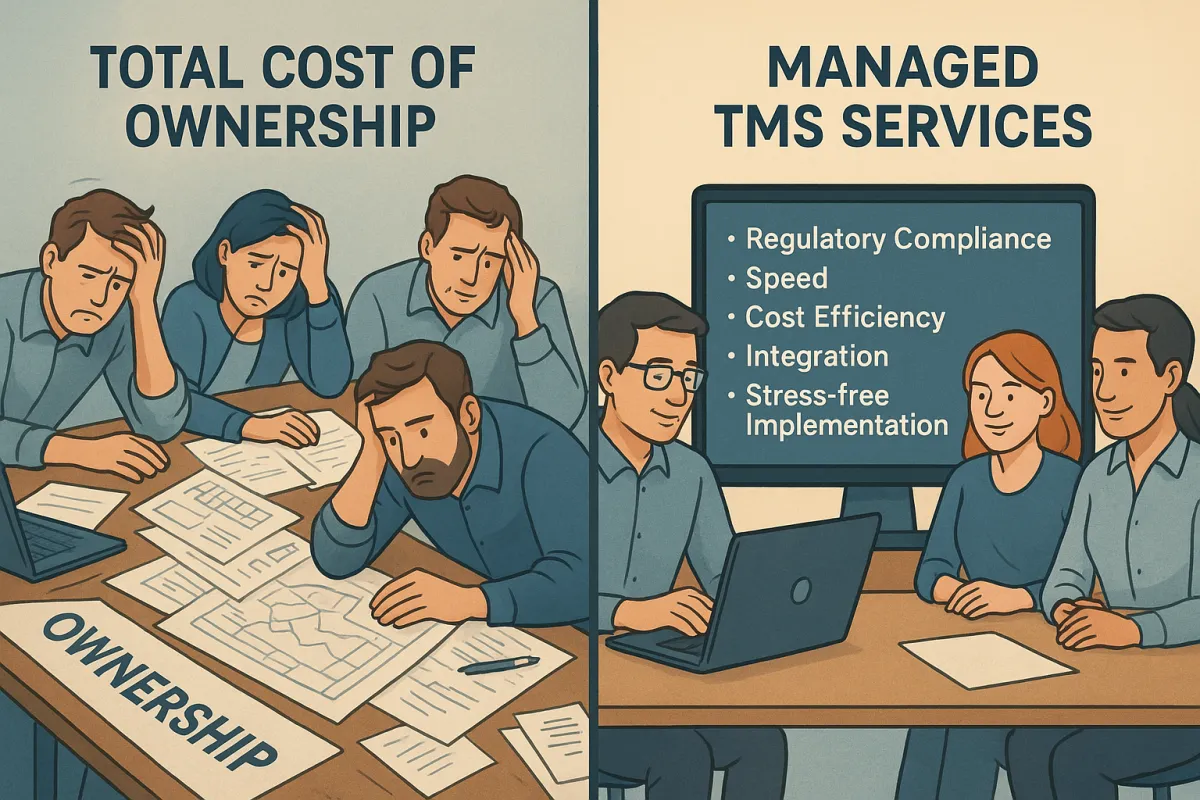

Managed transportation providers typically deliver 3-8% freight cost reduction via carrier network leverage, load optimization, and invoice auditing - savings that partially or fully offset the management fee. When you eliminate coordinator salary (replaced by oversight role), invoice leakage (provider responsibility), technology license (included in fee), and management time for data assembly, the total cost equation favors services for most mid-market European operations.

European Regulatory Compliance as Competitive Advantage

Europe's regulatory environment creates unique advantages for managed services approaches. Failure to comply with the regulations can result in severe penalties, which in some countries can reach up to 30,000 euros. The compliance burden extends beyond individual regulations to interconnected requirements that multiply integration costs.

Managed transportation providers absorb regulatory complexity as part of their service model. Start of application of the new version (v3) of ICS2 messages on 3 February 2026, and decommissioning of older version (v2) means your integration must handle messaging format updates automatically - work that managed providers handle within their service agreements versus custom development projects for traditional TMS implementations.

The procurement leverage works in your favor. Vendors need European reference customers for regulatory compliance capabilities. Any TMS contract signed now should include eFTI and Smart Tachograph compliance as baseline requirements, not optional upgrades. Vendors confident in their regulatory readiness will include compliance costs in base pricing.

Vendor Consolidation Risk Management

European procurement teams face unprecedented vendor consolidation pressure. WiseTech's acquisition of e2open for $3.30 per share in cash equating to an enterprise value of $2.1 billion marks the largest TMS industry acquisition to date, while Descartes Systems Group has acquired Columbus, Ohio-based 3Gtms for $115 million USD in cash.

Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams. When vendor acquisitions happen mid-implementation, your project timeline extends while support resources get redistributed. Traditional TMS procurement exposes you to integration risks you cannot control.

Managed services providers offer acquisition resistance through operational independence. When you outsource transport operations rather than licensing software, vendor ownership changes affect you indirectly rather than disrupting your daily operations. The services model provides natural protection against the consolidation wave reshaping the European TMS landscape.

Decision Framework: Software Versus Services

Your decision requires analyzing five critical dimensions rather than simple cost comparison:

Freight Volume Threshold: Managed transportation makes the most operational and financial sense for companies shipping 100-500+ loads per month with $2M-$30M in freight spend, a small internal logistics team, and more than 5 freight brokers to manage. Above €15M with dedicated logistics expertise, traditional TMS implementations can deliver higher operational control.

Internal Capability Assessment: Legacy ERP integration challenges hit mid-market companies disproportionately hard because they lack the internal expertise to manage complex system integrations. Services-led implementation approaches help bridge the expertise gap that destroys mid-market implementations.

Regulatory Complexity: European cross-border operations with multiple compliance requirements favor managed services due to provider expertise in regulatory integration. Domestic operations with simpler compliance needs can succeed with traditional TMS approaches.

Technology Evolution: TMS platforms that embed AI at the core, not as a marketing feature but as a fundamental part of how the system thinks, recommends, learns, and improves, will deliver compounding value. Evaluate whether your internal team can manage AI capability evolution or if provider-managed services offer better access to emerging technologies.

Vendor Selection Strategy: Platforms like Cargoson, Manhattan Active, MercuryGate, and Descartes each bring different approaches to ICS2 compliance, but European-native solutions often provide better understanding of cross-border complexity. Consider regional expertise alongside global scale when evaluating both software and services options.

Implementation Approach and Risk Mitigation

Your implementation strategy must account for compressed timelines and regulatory deadlines. Start core TMS functionality deployment by Q2 2025, ensuring carrier connectivity and basic operations function before regulatory deadlines create additional pressure. Cloud TMS implementations often conclude within eight weeks, compared to 6-18 months for traditional systems.

Phased approaches control both cost and risk exposure. Start with core functionality in Q2-Q3 2025, activate AI features in Q4 2025, and ensure eFTI compliance by Q1 2026. Managed services providers can execute this timeline without internal project management overhead, while traditional implementations require dedicated internal resources throughout the entire timeline.

Smart buyers negotiate carrier integration costs upfront and prioritize TMS providers with extensive pre-connected networks to control connectivity expenses. European-focused platforms often provide better value through pre-built carrier connections and regional expertise.

Success requires monitoring both technical and financial metrics. Monitor API response times, data synchronization success rates, and error frequencies alongside operational measures like carrier onboarding speed, compliance reporting accuracy, and cost savings achievement. European operations often see 15-25% improvements in transport administrative efficiency within the first year.

Your procurement decision framework must weigh total cost of ownership, implementation risk, regulatory compliance capability, and vendor consolidation exposure. Consider European specialists like Cargoson alongside global solutions, evaluating implementation methodology, regulatory expertise, and acquisition resistance as core procurement criteria. Whether you choose managed services or traditional software procurement, ensure your approach accounts for Europe's unique regulatory timeline and vendor consolidation pressures that will reshape the transport technology landscape throughout 2026 and beyond.