TMS Pricing Models Under Pressure: How Vendor Consolidation is Reshaping Cost Structures for European Procurement Teams

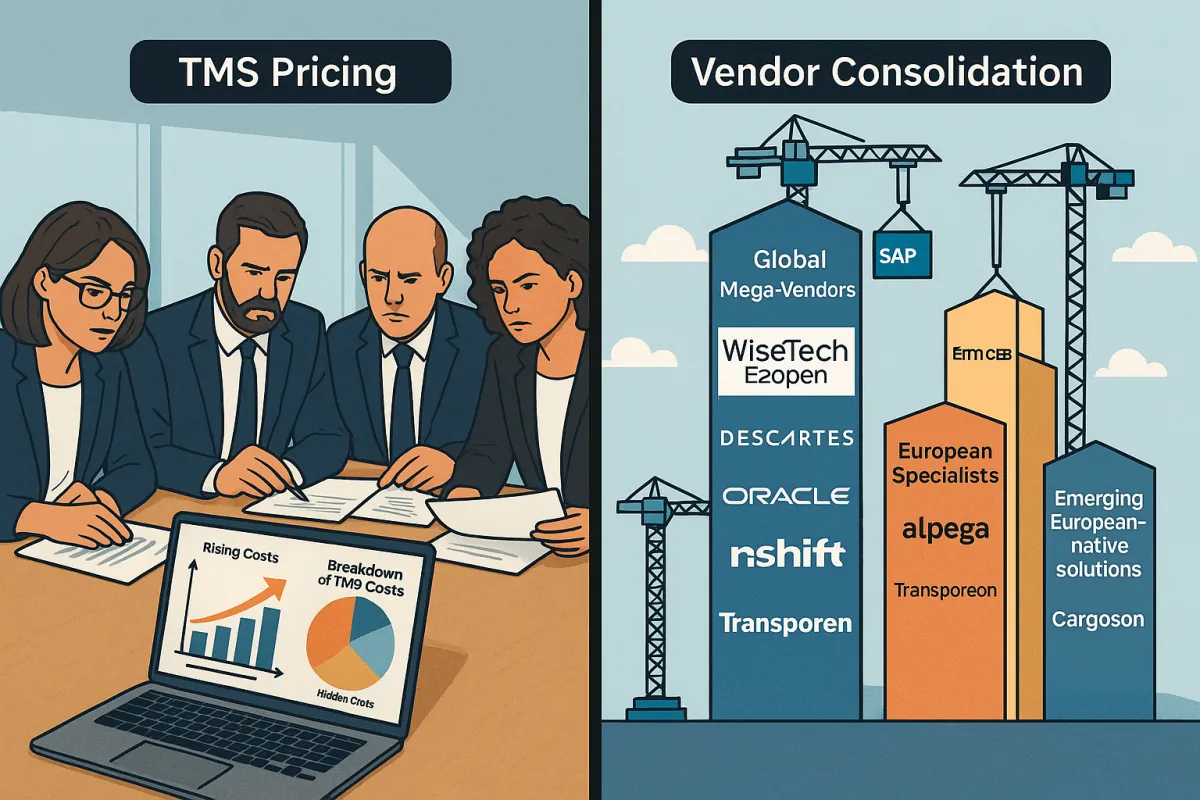

European procurement teams tasked with TMS selection face a perfect storm: WiseTech's $2.1 billion acquisition of E2open in 2025 and Descartes' $115 million purchase of 3GTMS represent just the opening shots in the largest vendor consolidation wave the industry has seen. Six months after implementation, actual costs exceed initial projections by 25-30%, with transaction-based TMS pricing ranging from €0.25 to €4.00 per shipment. The challenge runs deeper than sticker prices—it's about understanding how consolidation fundamentally reshapes the economics of TMS ownership.

The math becomes stark when you examine what European shippers actually pay. Cloud-based TMS software commonly runs from about $50 to $500 per user per month, with enterprise implementations often including setup and integration work in the $100,000 to $500,000 range. But those numbers tell only part of the story. For shippers with annual freight under management exceeding €250M, implementation costs often run 2-3x the subscription fees.

The New Economics of TMS Pricing in a Consolidated Market

WiseTech Global's $2.1 billion acquisition of E2open was fully debt funded and represents the largest in WiseTech's history, with the company leveraging experience from over 55 acquisitions to create a combined entity that fundamentally alters pricing dynamics. For e2open customers, the main concern is whether WiseTech will maintain innovation and product investment during integration, while for WiseTech clients, the acquisition offers broader supply chain capabilities but brings uncertainty about future product directions.

This consolidation creates three distinct market categories: global mega-vendors (including the combined WiseTech/E2open entity, Descartes, SAP TM, Oracle TM), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that focus specifically on cross-border European operations. Each category employs different pricing strategies that European procurement teams must decode.

When your TMS vendor becomes an acquisition target, you inherit integration risks without directly managing the project, with post-acquisition integration timelines typically spanning 12-18 months during which platform development stagnates while resources get redirected. This dynamic explains why purchase price represents only 20-25% of total cost of ownership.

Per-Shipment vs. Subscription Models: The Hidden Cost Analysis

European shippers receive pricing quotes that sound straightforward but hide significant complexity. Transaction fees can range from twenty-five cents to several dollars/euros per shipment depending on volume, while a good rule of thumb for top tier cloud TMS is anywhere from $1.00 to $4.00 per shipment, dependent on total monthly volume. The devil lives in the details that vendors conveniently omit during initial presentations.

Hybrid pricing models are gaining momentum, combining subscription and usage-based components. This trend reflects vendor attempts to balance predictable revenue with scalable cost structures. For European shippers, it means more complex TCO calculations that must account for seasonal volume fluctuations and cross-border complexity.

The integration layer adds substantial costs that transform initial pricing quotes into budget disasters. Basic API integrations cost €5,000-€15,000, while complex ERP connections exceed €50,000, with a basic domestic shipper requiring 10-15 integrations minimum, potentially totaling 1,000-1,500 hours of labor. More complex operations may need 140+ integration objects.

Consider how vendors structure their transaction models. Pricing based on documents and messages per shipment ranges from one cent to a few cents per transaction, but a shipment often triggers several or dozens of messages and documents, drastically increasing total cost and making budgeting difficult.

Regulatory Compliance Markups: The 2026-2027 Cost Explosion

European shippers face an unprecedented regulatory convergence that transforms TMS pricing calculations. The eFTI Regulation will apply in full from July 2027, with Member States authorities starting to accept data stored on certified eFTI platforms for inspection from January 2026. This creates an 18-month implementation window during which vendors can charge premium rates for compliance features.

A German automotive manufacturer signed a three-year TMS renewal without regulatory compliance pricing protection, and when their vendor introduced eFTI compliance as a premium add-on module nine months later, the additional licensing costs reached €800,000 annually. This case study illustrates why procurement teams should plan for 15-20% budget increases in 2026-2027 if reactive, or 8-12% if proactive with proper contract protection.

The regulatory burden extends beyond eFTI. From November 2025, with full implementation by June 2026, new dangerous goods transport rules take effect, while from July 2026, international freight transport performed by vans up to 3.5 tonnes enters the tachograph regime with mandatory G2V2 smart tachographs.

Post-Acquisition Pricing Risk Assessment Framework

For current e2open customers, the key question is whether WiseTech can maintain product investment and innovation while managing complex integration, while for WiseTech's existing clients, access to broader supply chain capabilities could be transformative. This uncertainty creates specific risks that European procurement teams must address through contract protections.

Smart contract negotiations include acquisition notification requirements, price protection clauses, functionality guarantees, and termination rights. Standard provisions should include 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights.

The integration complexity varies by vendor architecture. Legacy systems like SAP TM and Oracle TM dominate German operations but require extensive customization. European-native solutions like Cargoson and Alpega compete with faster regulatory response times and pre-built European carrier connections that reduce integration costs.

European-Specific Cost Considerations

Carrier integration complexity determines integration costs more than any other factor. The market includes established players like MercuryGate and Descartes alongside newer entrants like Cargoson, each with different approaches to transaction pricing, with some bundling visibility features into base rates while others charge separately.

European manufacturers typically work with 20-30 regular carriers but benefit from access to 200-300 qualified providers. This network complexity creates cost variations that standard pricing models don't capture. Regional vendors often provide better value through pre-built carrier connections and specialized European expertise.

Cross-border complexity multiplies costs in ways that single-market implementations don't experience. European shippers need systems that handle 27 different VAT rates, multiple languages, varying carrier integration protocols, and soon, mandatory eFTI compliance. European specialists like Cargoson and Alpega typically offer more transparent cloud-based pricing models designed specifically for European cross-border operations.

Building Acquisition-Resistant Cost Models

Successful TCO frameworks account for three cost layers: subscription/license fees, implementation costs that add 40-60% over the first two years, and operational costs for ongoing changes. Licensed TMS software costs $50,000-$400,000+ with annual maintenance fees, while platforms like Oracle TM and SAP TM exemplify pricing complexity through multi-layered fee structures including base licenses, user counts, transaction volumes, and regional modules.

Your vendor comparison methodology should evaluate base licensing, implementation services, carrier integration costs, training and support, and customization charges across realistic timeframes. TMS implementation usually takes 1-2 months for smaller shippers and 3-6 months for larger networks, with cloud TMS implementations often concluding within eight weeks compared to 6-18 months for traditional systems.

Timeline considerations become crucial when regulatory deadlines approach. The timeline provides an 18-month implementation window, but procurement and integration typically require 12-15 months for complex European operations, with Member State authorities accepting electronic information via certified eFTI platforms starting July 9, 2027.

Position modern alternatives including Cargoson alongside traditional vendors for balanced evaluation. European-native platforms often include compliance features as standard functionality rather than additional charges, providing better value for cross-border operations.

2026 Procurement Action Framework

The procurement window running through Q1 2026 provides optimal platform selection before consolidation eliminates choices, after which negotiation leverage disappears as regulatory pressure forces decisions. This compressed timeline requires immediate action from procurement teams still using traditional evaluation methods.

Use the eFTI preparation period as a vendor evaluation lever. Vendors claiming eFTI readiness should demonstrate functional integration by January 2026, not just promise compliance by the July 2027 mandate, allowing evaluation of actual implementation capabilities versus marketing commitments.

Risk mitigation strategies become essential when 66% of technology projects end in partial or total failure, with 17% of large IT projects threatening company existence. European procurement teams need acquisition-resistant frameworks that account for regulatory pressure, vendor consolidation, and implementation complexity simultaneously.

Start your assessment immediately. Procurement teams face a choice between rushing decisions to meet the window or delaying to face dramatically reduced options, with companies that haven't initiated TMS selection by mid-2026 finding significantly fewer viable options.

The convergence of vendor consolidation, regulatory requirements, and pricing complexity creates a narrow window for strategic TMS procurement. European shippers who act decisively in 2026 secure favorable contract terms and compliance-ready platforms before market consolidation eliminates their best options.